What is CPP? What’s the best time to take CPP? Plus more answers to all of your questions about CPP.

Originally published: October 19 2021

Updated: August 23, 2023

What is CPP? What’s the best time to take CPP? Plus more answers to all of your questions about CPP.

Originally published: October 19 2021

Updated: August 23, 2023

The Canada Pension Plan (CPP) is a social insurance program financed by payments from employees, employers, and self-employed individuals, as well as investment earnings. The CPP covers almost all working and self-employed Canadians, with the exception of Quebec, which has its own comprehensive plan, the Quebec Pension Plan. In case of retirement, disability, or death, the CPP replaces the contributors’ income. Find out how much CPP you’re entitled to at each age, whether it’s 60, 65, or 70.

A question I often get asked in my financial planning practice by those close to the start date age of the Canada Pension Plan (CPP) benefits is “Should I collect my CPP early?” The reality is that the answer is not as cut and dry as it may seem, and usually comes back to “It depends.”

There are several factors to consider: Do you require the additional income immediately? Are you still working and thus possibly in a higher tax bracket compared to retirement? Have you considered the opportunity cost and crossover age where waiting to take CPP made sense? There are answers to all of these questions and many more in our Comprehensive Guide to Canada Pension Plan (CPP).

In this article:

The Canada Pension Plan (CPP) is a social insurance program that helps contributors and their families when they retire, become disabled, or pass away. It provides a monthly, taxable benefit to replace your employment income, as well as some monetary compensation to the survivors of the contributors. It is an application-based benefit that you will receive for the rest of your life if you qualify, and to apply, visit the Canada.ca website. The amount of CPP you will receive is based on the contributions you provided during your working life.

Every employed individual in Canada who surpasses the minimum exemption threshold is required to make contributions to the Canada Pension Plan. Contributions are compulsory if you remain employed until the age of 65, and after that, they become optional until the age of 70 for those who choose to continue working.

You are guaranteed to get CPP when you retire. When you contribute to the Canadian Pension Plan, your money goes towards a fund that is used to pay out CPP upon your retirement. This money is only ever used for your CPP payment. A common misconception is that the CPP may go bankrupt because it’s a social insurance program, however, the federal and provincial governments have made changes to the program in the past to secure it for future generations to come.

In addition to the CPP retirement pension, you may also qualify for other CPP benefits. Like the CPP retirement pension, you will need to apply for these benefits.

If you continue to work and contribute to your CPP while receiving CPP payments and are under age 70, your CPP contributions will go toward post-retirement benefits (PRB), which will increase your retirement income with this benefit.

If you are under 65 and are not receiving CPP yet, and have a mental or physical disability that regularly stops you from doing any type of substantially gainful work, you might be eligible for this monthly benefit.

A benefit for those legally married to a deceased CPP contributor or the common-law partner of a deceased CPP contributor.

A benefit that provides monthly payments to the dependent children of disabled or deceased CPP contributors.

The death benefit is a one-time payment, payable to the estate or other eligible individuals, on behalf of a deceased CPP contributor; it is a $2,500 payment.

The Canada Pension Plan and the Canada Protection Plan share an abbreviation and are easy to confuse, however, they are very different entities. The Canada Protection Plan is a life insurance provider, which is in no way affiliated with the Canada Pension Plan. CPP (insurance) was recently founded but has grown to be one of the biggest insurance companies, especially for simplified life insurance . If you are looking to increase benefits for your loved ones upon your passing you can learn more about the best life insurance companies here . However, this article is covering the Canada Pension Plan; a social insurance program offering retirement benefits to those that qualify.

The CPP (pension) itself is involved in the life insurance industry through acquiring ownership of a subsidiary company, Ivari. Ivari has been providing life insurance for over 90 years and has an impressive financial strength rating; largely in part to the backing from the Canada Pension Plan itself.

The Canada Pension Plan is a social insurance program meant to provide safeguards for the contributor and their family in cases of income loss due to death, disability, and retirement. In order to apply you need to ensure that you:

The valid contribution to the CPP can be work you did in Canada or a result of receiving credits from a former spouse at the end of a relationship.

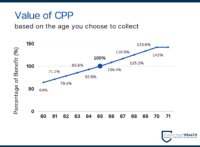

You become eligible to receive full CPP/QPP benefits starting from the initial month following your 65th birthday. Opting to wait until you’re 65 ensures you receive your full benefits, yet there’s an option to begin receiving them earlier, at 60. If you go this route, your benefits will be permanently reduced. Alternatively, you can delay receiving benefits until you turn 70, resulting in a permanent increase in benefits.

Similar considerations apply to individuals receiving Québec Pension Plan QPP benefits. If you’re aged 60 or older, it’s not necessary to have stopped working to receive your retirement pension from the QPP. You need a minimum of 1 year of contributions to the QPP. In cases where you’ve worked elsewhere in Canada, the QPP factors in your contributions to the CPP when determining your retirement pension amount. However, if you’ve had employment history in Québec, these earnings won’t be included in your CPP calculations.

Previously we listed qualifications to obtain any amount of CPP, but if you are looking to maximize the benefit amount you also need to ensure you have contributed to CPP for at least 85% of the time you are eligible to contribute.

In order for your contribution to count towards the number of years you contributed; you need to pay the amount calculated from the YMPE (yearly maximum pensionable earnings). Unfortunately, if you do not make enough income during that year; it does not count as a contribution.

The CPP is an application-based benefit, and you must apply if you want to receive it as the payments are not automatic. The Government of Canada recommends you submit the application prior to when you want your pension to begin, due to the processing time. Luckily, the application process is very straightforward and only involves 2 steps:

You will need your SIN (social insurance number) and relevant banking information on hand for the application. You may also need to include supporting documents alongside the signature page, but this will be specified in the online application. If you submit an application for CPP benefits post turning 65, Service Canada has the capacity to provide retroactive CPP/QPP retirement payments for a span of 12 months (comprising 11 months in addition to the month you apply). However, retroactive payments cannot be dispensed earlier than the month subsequent to your 65th birthday.

The Government of Canada recommends you apply well before when you want your first payment, and this is due to the varying processing times. Service Canada will begin to process your application upon receiving the application form. This may take up to:

It may take longer if you submit an incomplete application, and as they will require more information.

As mentioned above, there are many factors that go into the consideration of whether you qualify for the CPP benefits. If you meet the qualifications, you do not need to be worried about your application being denied. However, if your application is denied, you will have the opportunity to appeal to the Canada Pension Appeals Board and ask them to review your application. They will inform you if there are missing documents you need to provide to gain approval or tell you which requirements you do not meet.

You can take CPP as early as age 60, but you will receive fewer benefits than if you wait. For every month you begin collecting before your 65th birthday, there will be a reduction of 0.6%, accumulating to a yearly decrease of 7.2%. Opting to initiate pension collection at age 60 will result in a total reduction of 36%. If you wait until your 65th birthday, you will receive your full benefits. You can also choose to delay your benefits until age 70, which grants you extra benefits.

As with any financial plan, there are many risks associated with when you collect CPP. These risks include:

Not all these risks apply to everyone’s specific circumstances, but they are important to consider when deciding on your retirement plan. All 3 of these risks are decreased the longer you hold off on collecting CPP; as we can see through the relation between success rate and when you take CPP.

When reviewing retirement planning the success rate is measured by taking the retirement plan and comparing it with historical records of stock, bond and inflation rates. A plan is considered a “success” when it performs well with real-world returns. This analysis is by no means foolproof, but it does a good job of visualizing the decreased risk associated with delaying CPP collection.

Given an average CPP payment of $8,687/year at the age of 65, we can map out the success rate changes the later you collect CPP. For example, if you choose to collect your CPP at the age of 63, you will have a 53% chance of benefiting from your decision.

While the success rate does drastically increase as you delay collecting your CPP, this does not directly correlate to which age you should choose to collect. It is simply a good statistical measure to showcase the potential growth of CPP. Your decision should ultimately suit your personal retirement plan, and that is covered here.

The amount of your CPP retirement pension depends on different factors, such as:

For example, if you worked more than 40 years at the Yearly Maximum Pensionable Earnings (YMPE), you would qualify for the maximum CPP benefit. This benefit changes each year in January to match the cost of living, and for 2022, the maximum CPP at age 65 is $1,253.59 per month for new recipients. This value is subject to change depending on when you choose to collect CPP.

Talk to one of our experienced advisors today.

The value of the CPP benefit you will receive depends on when you decide to start collecting. If you choose to take CPP before the age of 65, you will face a 0.6% reduction for each month you collect before your 65th birthday, which is 7.2% per year. Whereas if you choose to take CPP at 70, you’ll have a 0.7% increase for each month after your 65th birthday, which is 42% more than if you started taking it at age 65.

This doesn’t necessarily mean that it’s better to take CPP at 65 or 70, because there are other factors to consider.

You can continue to work while receiving your CPP retirement pension. If you are between ages 60-70, you can still continue to contribute to CPP, which will go toward your post-retirement benefits and will increase your CPP retirement income payments. At age 70, your contributions to CPP will stop, even if you are still working (regardless of whether you are employed by a company or self-employed).

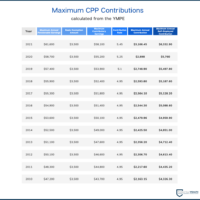

Your annual contribution is calculated by taking your annual pensionable earnings and subtracting the basic exemption amount (you can earn up to $3,500 of exempt income before you start paying the contribution). This value is your contributory earnings, and a percentage known as the contribution rate is then taken to get your final amount of annual contribution.

Employees in Canada who earn an annual income exceeding $3,500 are obligated to allocate 5.25% of their earned income, up to the predetermined maximum annual pensionable earnings, towards the Canada Pension Plan. Correspondingly, their employers are mandated to contribute an equivalent sum annually. In the province of Quebec, both employees and employers contribute to the QPP at a slightly elevated rate of 6.15% in the year 2022.

The minimum income requirement for contributing to CPP has remained unchanged for a long time (unchanged since 1996). However, the ceiling for maximum annual pensionable earnings is adjusted annually to accommodate the impact of inflation and the cost of living. In 2022, the maximum annual pensionable earnings have reached $64,900, marking a significant 5.3% increase, the most substantial rise since 1992, spanning three decades. Given the minimum threshold of $3,500, the highest individual income subject to taxation is capped at $64,900. The escalation in the contribution rate is attributed to the ongoing implementation of CPP enhancement.

If you are self-employed and/or run your own business, you are expected to pay the contribution rate as both an employee and an employer. This means your annual contribution will be double that of a standard employee.

YMPE (yearly maximum pensionable earnings) is the maximum amount of income used to calculate the contributions in relation to the Canada Pension Plan. In order to qualify for the maximum CPP benefit, individuals are expected to pay a percentage of the YMPE, known as the contribution rate, for at least 40 of their eligible years.

The CPP is currently going through an enhancement phase with the intention to make it easier for individuals to retire. For starters, there will be an increase in the CPP contribution amounts. The contribution rate has been steadily increasing since 2018, where it settled at 4.95% for the last decade. The most recent 2021 contribution rate was 5.45%, and the government is planning to continue the steady increase to 5.95% by 2023.

This increase in contribution rate will impact everyone equally and lead to CPP payments growing by almost 33%.

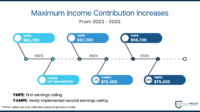

After an increase in the contribution rate, the government is looking towards increasing the income maximum. This increase will cap at 14%; being steadily phased in over 2 years starting in 2024. This change will only affect higher-income earners who are earning above the traditional CPP income maximum.

This higher ceiling will be called the YAMPE (year’s additional maximum pensionable earnings). Those who earn higher income will be expected to pay higher contributions but will be rewarded with higher payments upon retirement.

The CPP will also be implementing an additional factor to consider when calculating CPP. Younger employees who begin making contributions with the new CPP contributions will be given higher CPP payouts in the future; this means fewer savings will be required to reach a similar level of stability upon retirement. Older employees will receive a more modest increase as it will be proportional to how many years they contributed to the new CPP expansion.

The ideal age to start collecting CPP benefits varies depending on your specific circumstances. The standard age to take CPP is 65, but you may choose to take it out earlier at the age of 60 or later when you turn 70. Here are a few considerations to help you decide when to take out your CPP:

You have the option to start collecting CPP at the age of 60; prior to the standard 65. This is by no means a bad decision and may be beneficial to your retirement plans:

You get more income to enjoy your retirement earlier You have a longer period of time to collect the benefits You can put the excess income in investments You will not receive 100% of the benefit amount You may be put in a higher tax bracket which will negatively impact your Old Age Security benefitsSome things you should consider when deciding whether or not to take out your CPP early include:

You also have the option to start collecting CPP at the age of 70; later than the standard 65. This may be something to consider depending on your specific retirement plans:

You will receive a higher rate of benefit, meaning more income Your RRSP will grow steadily after the age of 70 You will not receive CPP income for the first 5 years of your retirement You will receive CPP for a shorter period of timeDue to the various factors at play, accurately predicting the amount of your CPP payment can be challenging. Before you decide when to take your CPP retirement pension, you should consider:

Every circumstance is different and requires discussion and analysis. Although rare, someone may like the idea of receiving the maximum government pension instead of taking it at an early age or at age 65. Why? They may have a registered retirement savings plan (RRSPs) to supplement the income they would receive from CPP and lock in a benefit that is 78% higher at age 70 compared to taking it earlier at the age of 60. That being said, you may decide that they would rather have the income immediately rather than wait.

If you still have questions about if Canada Pension Plan is right for you, check out the Frequently Asked Questions (FAQs) that people have about CPP.

The Canada Pension Plan is considered income, therefore it is indeed taxable. Although taxes are not deducted automatically, you can request to have it deducted from your monthly payment.

Yes, you can continue to work while receiving your CPP retirement pension. If you are between ages 60-65, you must continue to contribute to CPP, which will go towards a post-retirement benefit and will increase your CPP retirement income payments. If you’re working at the age of 65-70 you can choose to not contribute to CPP. At age 70, your contributions to CPP will stop, even if you are still working (regardless of whether you are employed by a company or self-employed).